The Dallas-Fort Worth (DFW) area ranked first in the U.S. commercial real estate market for 2026 by both the PwC and the Urban Land Institute. This was based on factors such as continued corporate relocation, population growth and a stable, business friendly economy. The DFW metroplex currently has the second-largest financial services workforce in the United States and is seeing an increased demand for high-amenity Class A office space and infill industrial assets. For institutional investors and corporate occupiers looking to work in this rapidly changing market, it is important to have a brokerage partner who can effectively navigate the local capital markets and has experience with complex site selection. These capabilities are typically found among the top real estate companies in USA.

The current real estate environment is influenced by a flight to quality, where premium submarkets such as Uptown continue to see rent growth even as the broader market experiences instability. In this environment, commercial brokers are increasingly using AI-driven analytical tools to analyze site-specific factors that influence tenant demand, such as access to labor and logistics, particularly in large metropolitan areas such as Dallas-Fort Worth. Knowing how these micro-markets work helps when negotiating lease terms, especially as tenant improvement allowances and free rent are becoming more important in 2026.

Choosing the right broker in North Texas is about finding a professional with the experience to fit your unique needs whether it’s urban-industrial, grocery-anchored retail or office space. The firms listed below are the leaders in the field of Dallas commercial real estate and provide both the institutional scale and local knowledge required to achieve maximum ROI. This guide will take you through the top power brokers and the current economic factors that are positioning Dallas as a leading market for global real estate investment.

See how a dedicated CRM helps Dallas commercial firms manage high-volume leasing pipelines, automate TI allowance tracking, and stay ahead of the flight-to-quality trend.

Explore CRM

This table features eight powerhouse firms dominating the North Texas commercial sector, ranked by local leasing volume, square footage managed, and specialized asset expertise.

Talk to a Dallas CRE expert

Quick Chat

1

CBRE

Website: cbre.com

Headquarters: Dallas, TX (Uptown)

Established Year: 1906 (Global HQ moved to Dallas in 2020)

Key Person: Bob Sulentic – CEO

Core Services: Investment sales, agency leasing, valuation, and debt/structured finance

Awards: Ranked #1 in DFW for local square footage managed and leasing volume by Dallas Business Journal

2

JLL (Jones Lang LaSalle)

Website: us.jll.com

Headquarters: Dallas, TX

Established Year: 1783 (Global)

Key Person: Jeff Ellerman – Vice Chairman (Dallas)

Core Services: Tenant representation, industrial property management, and AI-driven market analytics

Awards: Recognized for the highest local leasing volume in North Texas with over 31 million sq. ft. moved

3

Cushman & Wakefield

Website: cushmanwakefield.com

Headquarters: Dallas, TX

Established Year: 1917

Key Person: Doug McKnight – Managing Principal

Core Services: Multifamily advisory, sustainability consulting, and global occupier services

Awards: Top-ranked for logistics and retail sector expertise in the DFW metroplex

4

Stream Realty Partners

Website: streamrealty.com

Headquarters: Dallas, TX

Established Year: 1996

Key Person: Chris Jackson – President

Core Services: Industrial development, property management, and urban office leasing

Awards: Second-largest managed portfolio in North Texas with over 68 million sq. ft. under management

5

Newmark

Website: nmrk.com

Headquarters: Dallas, TX

Established Year: 1929

Key Person: Gary Carr – Vice Chairman (Capital Markets)

Core Services: Institutional investment sales, debt placement, and creative deal structuring

Awards: Leader in high-volume institutional sales for data centers and logistics hubs

The Dallas-Fort Worth metroplex has solidified its position as the top market for real estate investment in the United States for 2026. This growth is sustained by a diverse economy, a business-friendly climate, and massive infrastructure projects. Key drivers include:

- The emergence of Dallas as a leading financial center, anchored by the new Texas Stock Exchange, attracts institutional capital and professional services.

- A continuous wave of corporate headquarters relocations seeking lower operating costs and a deep, specialized talent pool.

- Expansion of the inland port and logistics hubs near DFW International Airport fuels unprecedented demand for industrial and data center space.

- Major investments in the Highway 121 corridor and the Silver Line rail project enhance connectivity between suburban growth engines and the urban core.

Source: PwC, ULI, Dallas Business Journal

Source: Weitzman, Cushman & Wakefield, NAI Robert Lynn

Talk to a Dallas CRE expert

Quick Chat

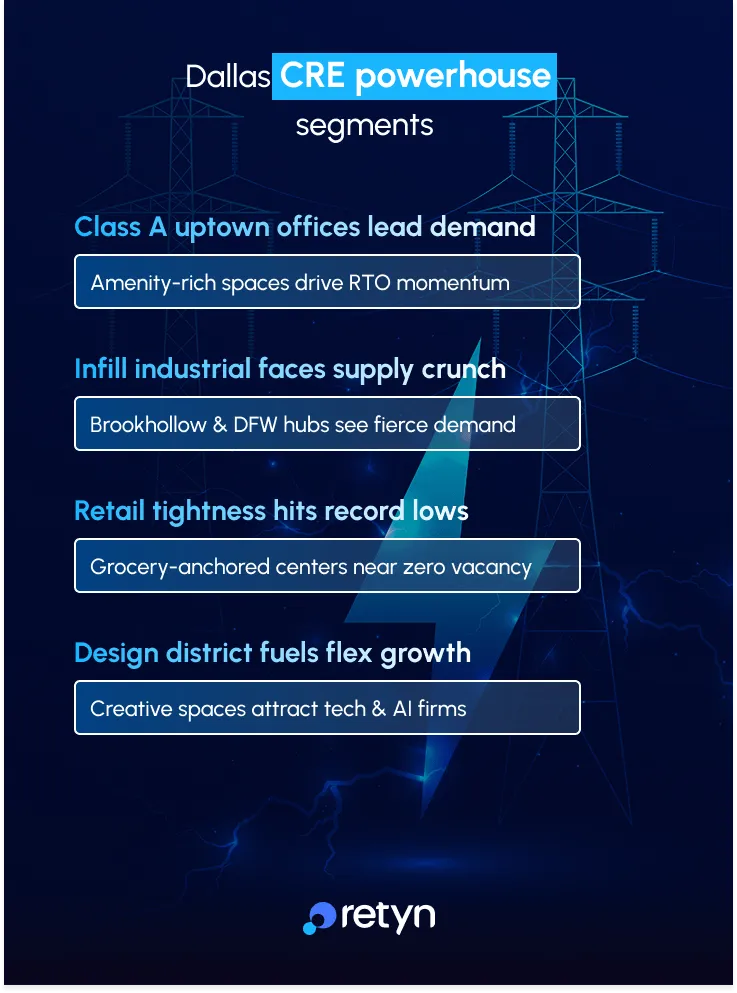

The DFW market is segmented into specialized hubs, each requiring a broker with deep local leverage and specific asset knowledge.

- Occupiers seeking Class A space in Uptown prioritize amenitized buildings to drive employee return-to-office initiatives.

- Infill industrial assets near Brookhollow and DFW Airport are seeing intense competition due to limited land and surging last-mile delivery needs.

- Retail remains the tightest sector, with grocery-anchored centers in suburban corridors maintaining near-zero vacancy.

- Creative flex spaces in the Design District are increasingly popular for tech and AI firms requiring a mix of office and showroom capabilities.

Institutional and private investors are capitalizing on the region's pro-business regulatory environment and strong yield potential.

- Landlords are currently offering record-high Tenant Improvement allowances, often exceeding $100 per square foot for long-term trophy leases.

- Texas has no state income tax, which significantly enhances the net operating income for commercial property owners compared to coastal markets.

- Significant free rent periods of 6 to 12 months are currently negotiable for large-scale corporate relocations and renewals.

Despite record-breaking growth, the scale and speed of the North Texas market create distinct operational hurdles for property firms.

- The bifurcation of the office market creates a surplus of older, non-amenitized space that requires creative adaptive-reuse strategies.

- Rising construction costs for specialized build-outs put pressure on Tenant Improvement budgets and lease negotiations.

- The rapid pace of corporate relocations demands real-time data accuracy to prevent clients from losing prime sites to competitors.

- Increased competition for top-producing brokers leads to frequent poaching between global giants and local boutique firms.

Dallas brokerages are leading the nation in adopting PropTech to streamline the complex lifecycle of commercial transactions.

- AI-driven site selection tools analyze commute patterns and talent density to identify the optimal headquarters location.

- Digital twin technology and virtual 3D tours allow international investors to inspect industrial assets without traveling to DFW.

- Automated lease administration platforms help firms track expirations and renewal options across massive regional portfolios.

- Advanced CRM systems now integrate directly with local tax and zoning databases for faster due diligence.

Success in the 2026 Dallas commercial market requires a blend of hyperlocal insight and modern automation. Firms that utilize data-driven platforms to manage their pipelines will be better equipped to handle the high-volume environment of the North Texas financial hub. As the region continues to outperform national benchmarks, the brokers who embrace tech-forward tenant representation and agile property management will dominate the landscape.

A real estate growth platform provides the infrastructure necessary to scale your brokerage, from automating compliance to enhancing the institutional investor experience.

Empower your Dallas brokerage to manage every lease and capital market lead with AI-powered efficiency.

Get CRM now

FAQs on navigating Dallas commercial real estate

With Dallas’ flight-to-quality trend, landlords are incentivizing their top tenants to sign longer term leases at Class A office properties. TI allowances generally fall in the $30 to $50 per square foot range, though some Class A properties may offer higher allowances. Landlords may also provide additional concessions such as free rent to attract tenants.

A traditional full-service broker works on behalf of either the landlord or the tenant. Working in this capacity may create a conflict of interest when negotiating occupancy terms with other parties. A tenant-only firm (such as Hughes Marino or Cresa) works exclusively on behalf of occupiers, so your broker’s priority is to reduce occupancy costs rather than find tenants for landlords.

- Triple Net (NNN) - Most common in retail and industrial properties, with the tenant paying base rent as well as all property taxes, insurance and maintenance costs.

- Full Service Gross - Most common in high-rise office buildings. The landlord will pay for operating costs and bundle them into a single predictable monthly payment.

The launch of the TXSE in downtown Dallas is contributing to the city's transformation into a major financial hub. This is supporting demand for trophy office space in the Uptown and Turtle Creek submarkets.

Yes. Vacancy rates have increased in several areas of the office market. As a result, to attract tenants, many landlords continue to provide free rent and other concessions for new leases. Across major U.S. office markets, free rent is typically provided for an average period of eight to nine months.

The Dallas North Tollway corridor, including Plano and Frisco, is one of the key hubs for corporate headquarters, supported by large office campuses and access to a strong professional talent base.

Industrial property vacancy rates ranges from 8-10 percent within the Dallas-Fort Worth area (including areas near DFW Airport). Smaller industrial buildings typically under 50,000 sq. ft. tend to be in higher demand than larger industrial buildings, which means they generally have a lower vacancy rate.

Disclaimer: Retyn does not promote or endorse any company listed above. The firms mentioned are selected based on 2025/2026 market volume and public data. Data is subject to change based on market fluctuations.